Embedded Finance: How Financial Services are Reshaping B2B Ecosystems

In the UK market, two contrasting trends stand out. In 2024, 67% of shoppers abandoned an online purchase due to friction during the checkout process, according to Mastercard.¹ Yet, at the same time, digital and online payments are gaining ground: cash usage has dropped from 23% of all payments in 2019 to just 9% in 2024, and 57% of adults now use mobile wallets, according to UK Finance.²

Meanwhile, instant account-to-account (A2A) payments account for around 7% of e-commerce transactions, a share that continues to grow.³ In short, demand is clearly shifting toward more digital experiences — but the checkout “bottleneck” still costs valuable conversions.

Why do these figures point to Embedded Finance? The growth of electronic and instant payments shows that users value seamless processes; high abandonment due to payment issues demonstrates that any interruption outside the flow penalizes conversion.

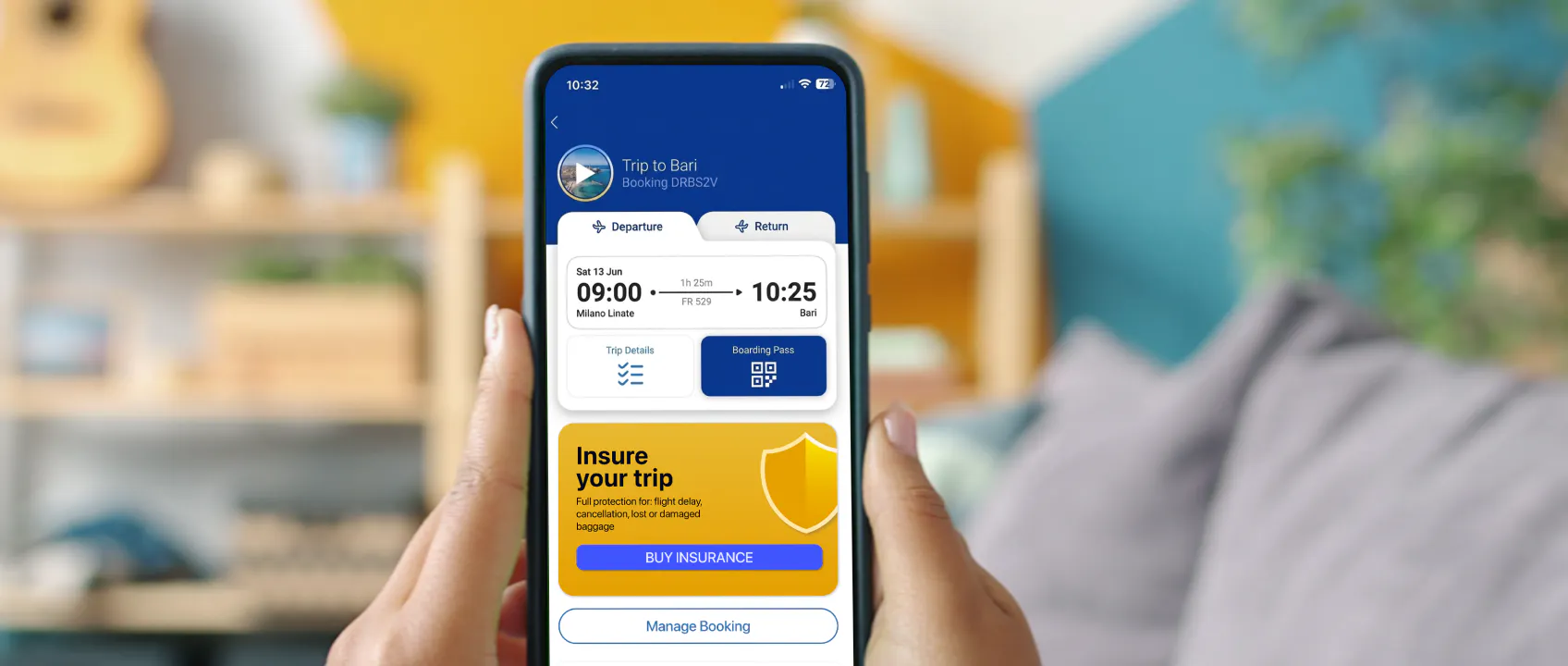

This is where Embedded Finance plays a key role. It is not about “adding one more payment method,” but about integrating financial services directly within the flow where the decision is made, with the goal of offering a complete experience: paying, financing, insuring, or verifying without leaving the point where the user—consumer or business—is already acting.

And while the benefits in B2C are clear—faster, frictionless purchases—in B2B, the impact is structural.

From Chain to Ecosystem: How Embedded Finance Transforms the B2B Value Chain

In B2B, the traditional financial value chain is linear: the regulated entity creates the product, distributes it through its own channels, offers it to the user, and manages post-sale services. Embedded Finance breaks that sequence and turns it into an ecosystem where multiple actors contribute value in parallel: for the user, the visible component is the core service (an eCommerce platform, a mobility app, a healthcare portal…), while the financial components (payments, financing, cards, and insurance) are transparently integrated into the customer journey—providing exactly what is needed, where and when it is needed.

What changes with Embedded Finance:

- Production (manufacturing): The regulated entity (bank/PSP, lender, insurer, identity provider) continues to produce financial services (accounts, payment infrastructure, credit, policies, KYC/KYB), assuming licensing, risk, and compliance. What changes is not who manufactures, but where it is consumed.

- Distribution: The non-financial company (marketplace, supplier portal, company in another sector) integrates and orchestrates financial services within its customer journey, under its own brand and business logic, becoming a distribution channel.

- Usage: The financial decision happens within the main journey. While the user completes a purchase, they can choose to pay via Pay by Bank, accept financing, add a personalized insurance policy, or process a KYB verification—all without leaving the experience.

- Service (post-sale): Responsibilities are shared between the regulated entity (claims, defaults, disputes, regulatory requirements) and the distributor (experience and communication within its own portal).

The Value of the B2B Ecosystem: The Case of Embedded Data & Risk

To understand how Embedded Finance can also transform risk assessment and management processes, consider the case of a utilities company that integrates an Open Banking–based scoring system directly into its onboarding flow. With the customer’s consent, account data is retrieved via an Account Information Service Provider (AISP) license and assessed through a credit risk model developed by external providers.

What changes for the parties involved?

- Utility company: Improves customer acquisition by approving profiles with limited or no credit history, reduces exclusion, and accelerates service activation.

- AISP provider: Gains recurring, consent-based access, improves connection coverage and reliability, and can offer complementary services (account verification, Verification of Payee – VoP) with steady revenue streams.

- Risk model provider: Gains access to transactional data, allowing for enhanced predictive models and expansion into new sectors.

- Bank or payment provider: Benefits from more accurate risk signals to anticipate defaults, reducing bad debt and operational costs.

- End customer: Can contract the service quickly and easily—even without credit history—directly from the app, with a smooth and continuous experience.

The Advantages: Acquisition, Payment Reconciliation, and Operational Efficiency

The Embedded Finance market shows strong growth confirming the effectiveness of ecosystem-based models. Its global market is expected to rise from USD 110 billion in 2024 to USD 1.7 trillion by 2034, with a CAGR of 31.53%.⁴ Moreover, 67% of organizations surveyed by Forrester in 2025 anticipate over 30% year-over-year growth in indirect revenues—those generated through partnerships.⁵

For financial institutions, Embedded Finance completely revolutionizes the business model, opening the door to multiple revenue streams:

- Improved acquisition: Offering the right option at the right time (method, rail, terms) increases collection rates and reduces abandonment in complex B2B flows.

- New revenue streams: Activating upsell and cross-sell of embedded financing and insurance at the decision point increases the value of each transaction, diversifies revenue, and raises ARPU without adding friction.

- Operational efficiency: Real-time confirmation, automatic metadata reconciliation, and the use of A2A payments reduce per-transaction costs, minimize accounting errors, and shorten DSO.

- Reduced onboarding friction: Integrating Identity/KYC/KYB based on risk levels maintains the manufacturer’s regulatory standards while offering a fast, traceable UX directly from the platform.

- More predictable cash flow: By sharing signals across ecosystem participants and operating with real-time data, companies improve liquidity forecasting, anticipate defaults, and gain operational resilience.

For non-financial companies, Embedded Finance is both a growth driver—enabling commission-based revenue from bundled sales—and a loyalty booster. Offering a seamlessly integrated financial service—whether an instant payment, one-click approved loan, or personalized insurance coverage—dramatically enhances the experience and encourages customers to stay within the company’s ecosystem, increasing Customer Lifetime Value by 2–5 times and reducing customer acquisition costs by up to 30%.⁶

The European Embedded Finance Landscape

The EU has not overlooked the transition toward ecosystem-based business models. It is developing a coherent framework acting as a “common foundation” to scale Embedded Finance across the Union through four key regulatory levers:

- Instant Payments Regulation (IPR)

- Verification of Payee (VoP) – IBAN-name matching

- Payments package (PSD3 / PSR)

- Financial Data Access (FIDA)

These initiatives pursue a dual objective: on one hand, regulatory harmonization, with standard, interoperable rules for payments, data sharing, security, and fraud prevention to facilitate cross-border integration among European players; on the other, infrastructural enablement, creating reliable and shared “technological rails” upon which banks, fintechs, and non-financial companies can orchestrate embedded financial services at scale.

UK in Focus: Embedded Payments Paving the Path to Embedded Finance

Within the UK framework, embedded payments riding on Faster Payments and Open Banking rails are a practical bridge to Embedded Finance: they cut checkout friction, support clean reconciliation with structured references, and add strong anti-fraud signals through name-checking via Confirmation of Payee (CoP)—now covering over 99% of organisations initiating Faster Payments.⁷ In consumer channels, momentum is increasingly driven by Open Banking “Pay by Bank”: 31 million open-banking payments were recorded in March 2025 and users reached 15.16 million in July 2025, indicating rapid mainstreaming; even so, A2A’s e-commerce share sits around 7%, underscoring room to grow.⁸ ⁹ On the B2B side, Pay.UK’s Request to Pay service enables invoice-linked, data-rich requests that streamline collections and reconciliation, and ongoing UK policy moves—most notably the APP-fraud reimbursement regime (effective 7 Oct 2024)—reinforce trust and adoption without sacrificing user experience.¹⁰

Looking Ahead: AI and Embedded Finance – From Payment to Prediction

At a time when artificial intelligence is transforming how we live and work, one thing is clear: the next step in Embedded Finance lies in its integration with AI technologies.

AI will increasingly make it easier to read the ecosystem’s pulse—payments, invoices, inventories, incidents, behaviors—and detect where and when to integrate additional financial services: order-based financing, contextual insurance, instant A2A payments with VoP, split and dynamic payouts.

The next wave of Embedded Finance will therefore be predictive: AI will turn scattered signals into real-time decisions, driving the shift from static ecosystems to adaptive ones that evolve in sync with the market and its participants.

To sustain a business model where connections and multichannel are the backbone, companies will need orchestration-ready infrastructures. Payment orchestration platforms like Fabrick Payment Orchestra can be decisive allies: they enable agile growth, routing and optimizing payment rails, applying risk and compliance rules, normalizing APIs, and logging events—improving conversion, reducing DSO, and enhancing experience in a constantly changing market.

Sources

“67% of UK shoppers abandon online purchases due to checkout friction” | Mastercard, 2025

UK Payment Markets Summary | UK Finance, 2024

A2A payments in the UK: why consumer adoption lags and how to fix it | UK Finance, 2024

Embedded Finance Market Set for Rapid Expansion as Digital Integration Transforms Financial Services | Precedence Research, 2025

The State Of Partner Ecosystems In 2025 | Forrester, 2025

Embedded finance: How banks and customer platforms are converging | McKinsey, 2024

Confirmation of Payee: the journey so far | Pay.UK, 2025

OBL Impact Report 7 | Open Banking Limited, 2025

A2A in UK: ~7% of e-commerce | UK Finance, 2025

PS24/7 policy statement: APP-scam reimbursement | Payment Systems Regulator, 2024

Our insights

Embedded insurance: how integrated insurance platforms are reshaping distribution

How AI is reshaping financial services: key trends, applications and business impact